How to sell a business?

Do you think it's high time to sell your business?

Maybe you have never done this kind of thing before. So, know that there are quite a few factors to consider throughout the process (from logistics to the moment of sale).

First of all, you should know that selling a business is a very common practice among entrepreneurs. I understand that some people may have a little trouble with this concept, and yet, it is something completely normal!

The reasons for this sale can be numerous. Some do it because they are about to retire, while others are simply overwhelmed and prefer to sell their business. There are those who are preparing to live another chapter of their life.

Whatever the reason, you must adopt the right approach when selling your business. The profits you will make from it should allow you to build another business or even better: give you the financial freedom you have always dreamed of.

Now, I know what needs to be done to sell a business in the right way. Indeed, the sales processes may seem complicated, but I have simplified them into 5 steps for you.

Step 1: Evaluate your business

Most entrepreneurs think they have an idea of the value of their business. But in many cases, the number they have in mind is very different from its actual value.

Before setting a price that is too high or too low, it is therefore preferable to consult with an evaluation expert. An evaluation by a third party will indeed give you a more realistic estimate. They will then provide you with a detailed report regarding this estimation.

If potential buyers ever question the value of your business, you can simply share this report with them. It will make the estimate more credible. At the very least, the evaluation will give you an approximate idea of what you can expect.

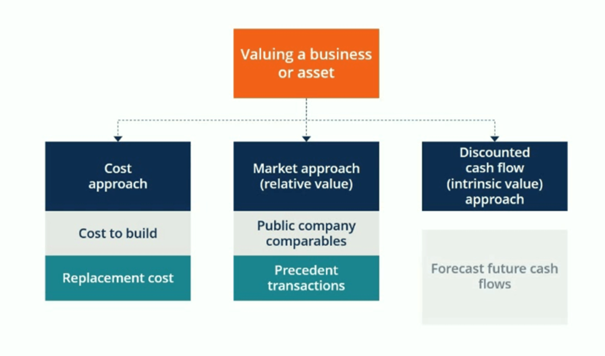

In case you do not want to hire an expert, you can always try to determine the value by yourself. In general, there are three main ways to evaluate a business: the cost approach, the market approach, or the intrinsic value approach.

The third method, also known as the discounted cash flow approach, is the easiest to implement. Most businesses are typically valued between three and six times the current cash flow.

That being said, there are many other factors to consider here:

industry trends

endettement de l’entreprise

actifs et entreprises similaires à vendre

et bien d’autres

Whether you estimate the value yourself or you hire a third-party appraiser, remember that it is only an "evaluation". It may not necessarily be the final selling price.

In the end, a company is only worth what someone is willing to pay for it. If you are not satisfied with the evaluation, maybe it is not yet time to sell the company?

Moreover, one can simulate selling a business to selling real estate. Your real estate agent could tell you how much the house is worth, but the property could remain on the market for months at that price.

And to increase the value of the property, an investment would be welcome!

Step 2: Get your finances in order

Once you have determined the value of the company, it is time to organize your finances. For some of you, this will be much easier than for others.

Selling a business highlights your financial history. Potential buyers, lawyers, accountants, third-party valuation companies, brokers, specialists, and other individuals will closely examine your records. For everything to go smoothly, your accounting must be impeccable.

In general, you will need to provide at least the last three years of tax returns, as well as accurate financial statements (balance sheet, income statement, cash flow statement).

Any error or disorganization in these files could be a warning signal for potential buyers. Inconsistencies in your books could raise other questions

Am I being misled?

Ces chiffres dissimulent-ils quelque chose ?

Puis-je croire tout ce qu’on m’a dit d’autre sur l’entreprise ?

Etc.

Put yourself in their shoes; you will understand better.

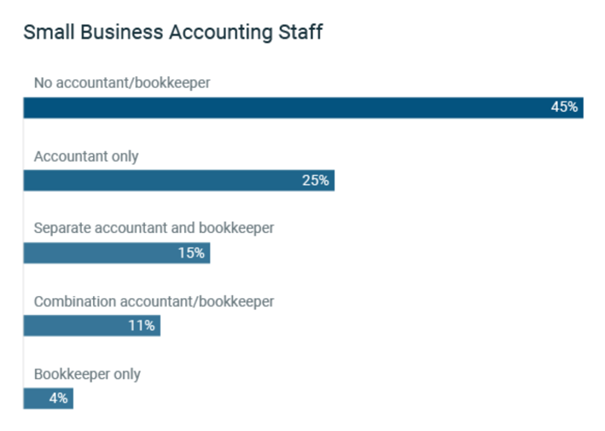

However, the vast majority of small businesses do not have an accountant; they also do not keep accounting books.

And you? Do you not have one either? If that's the case, I strongly recommend hiring an accountant. It will greatly simplify your life in the future.

Step 3: Hire a business broker

Now that everything is ready, two options are available to you:

Selling a business on your own

Faire appel à un courtier

This first option is feasible if you are selling the business to someone you know very well (perhaps a family member or another trustworthy person). At the same time, you save a lot of money (especially on brokerage fees)...

On the other hand, the second option is the most popular.

Will there be any additional fees associated with this method, you ask? Absolutely. But a broker can help you get the best possible price and sell your business faster (compared to if you were to sell it yourself).

Brokers also work on commission. It is therefore in their interest to sell a company at maximum value.

However, the broker still takes the time to establish their own evaluation of the company. This does not mean that you should neglect the estimate you made in step 1. It is true that the two numbers may not necessarily be the same, but it would be truly better if they are relatively close.

In case the difference is too significant, why not seek a third opinion? This will help you determine which of the two numbers is more accurate.

Brokers have a wealth of experience in selling businesses, which is extremely important. Here are some other examples of tasks they will need to take into account:

Find the best buyers

Promotion de la vente

Assurer la confidentialité

Obtenir un financement

Aider aux négociations

Gérer la diligence raisonnable

Dans quel délai vendre une entreprise ?

More precisely, how much should the services of a broker cost? As I mentioned earlier, a broker earns money through commission. So, it depends on the price of the business, but also on what your business earns.

You must know this rule: the higher your income, the lower the broker's commission fees.

A company with a turnover of less than 1 million dollars generally pays brokerage fees of 10 to 12%, while companies with a turnover of over 25 million dollars pay a commission ranging from 2.5 to 4.5%.

Step 4: Find prequalified buyers

Selling a business is clearly not easy. At some point, you will be required to disclose sensitive information about your company. Your competitors will be happy to collect them!

Indeed, it is possible that a competitor, or someone acting on behalf of a competitor, may pretend to offer a deal with the sole purpose of examining your finances. Therefore, you should never disclose this kind of information to anyone.

One must sort the prequalified buyers.

Also, do not get too excited about the first offer you receive and do not assume that the company will be sold. In fact, it takes an average of 6 to 8 months to sell a business.

The broker is not the only professional you can trust. There are also sales experts who can help you accelerate the selling process. Being experts, they also know how to pre-select potential buyers.

I will show you a trick:

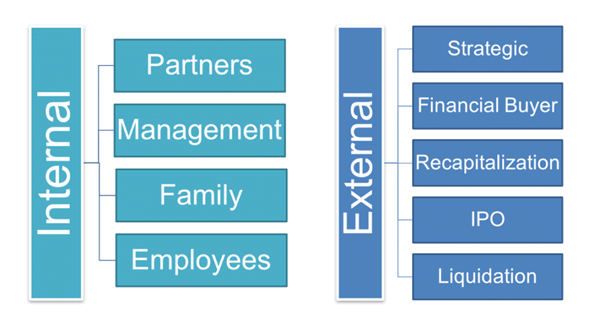

Buyers can generally be segmented into three main categories:

Individual buyers

Acheteurs stratégiques

Groupes de capital-investissement

However, the type of buyer making an offer plays a role in the time needed to process the transaction. For example, an individual buyer will likely need a bank-secured loan, which approval can take up to 90 days. On the other hand, a private equity group may fund the purchase themselves.

Do not rush to accept an offer right away. You can always use one offer to trigger another, which will allow you to get the maximum value for your business.

Step 5: Finalize legal documents and contracts

Once you have found a qualified buyer and accepted an offer, it is time to finalize the deal.

This is where things get a little complicated. Hence the need for a lawyer!

Among the legal documents and standard contracts associated with a business sale, we can mention:

A purchase contract

Une liste des actifs

Des accords de non-concurrence

Les lignes directrices pour l’utilisation des sites web et des noms de domaine

Un acte de vente

Un accord de sécurité

There are those who write their own contracts, and yet, it's a very bad idea! You could miss vital information, and as a result, you will be vulnerable in case of unforeseen circumstances. Especially since contracts typically contain between 25 to 50 pages.

If your current lawyer is not an expert in contract law, he should be able to recommend a colleague to you.

Once everything is in order, all that's left to do is sign.

Other tips and practices for effectively selling a business

Although the process of selling your business can be simplified by limiting it to the five steps listed above, there are certain things you must do to ensure that everything goes smoothly.

1. How to keep your business in good condition?

As I have already mentioned, selling your business takes time. You cannot expect to receive an offer overnight.

So do not make the mistake of neglecting your business during the period of its sale. I have already met business owners who put so much effort into selling their business that they ended up neglecting the business itself.

You must think about both sales and business management.

As long as the company is performing well, its value continues to increase. It will only attract buyers. On the other hand, a decrease in productivity is considered an important warning signal for potential buyers.

I recommend using software to help maximize your productivity and that of your team

If you lead a team, know that the application of the

I repeat: it is important to seek help (especially from professionals such as brokers, lawyers, accountants...). You need to know what is important, and act accordingly.

2. Why are exit strategies important?

Every business owner must have an exit strategy. But did you know that an exit strategy must be developed well before the sales stage?

It was necessary to plan for it before anything else. In fact, implementing such a strategy requires time. If you haven't thought about it yet and you are about to sell a business, I prefer to stop you.

First, dedicate time to setting up the strategy, as it also helps to sell a business quickly and in the right way.

But then, what do you do if you find yourself in a situation where you absolutely have to sell your business?

A major competitor has entered the market

Vous n’arrivez plus à vous occuper de l’entreprise

Vos enfants ne veulent pas vous remplacer, et l’entreprise ne survivra pas

These are just examples of cases that could arise.

You do not have time to establish an exit strategy, and as a result, you will certainly not be able to sell a business at the maximum price.

It is therefore necessary to put in place an emergency plan for a wide range of possible exit strategies.

3. Logic should prevail over emotions

Selling a business can be emotional, especially when it is a family business or a small business. To get to where you are now, you have probably worked extremely hard; in fact, this is something that all entrepreneurs have in common.

That being said, do not let your emotions take over. It will cloud both your thoughts and your decisions.

Also know that potential buyers do not care about the number of hours you have worked per week over the past 10 years. All they are interested in is the end result. If you think they are offering a too low or unfair offer, you are free to refuse it.

In other cases, a competitor may make a legitimate and fair offer, with the full intention of buying. Don't let an old rivalry prevent the deal from happening.

Should we require payment in advance or not?

Make sure that the terms of your agreement include an initial payment. Some buyers may make you a tempting offer, but do not have the means to pay you right away.

Getting paid over time may not seem very important, but this arrangement could cause you some problems in the future. You could find yourself in a situation where you are not being paid according to the terms you agreed to. In this case, any legal action would only add an extra expense to your budget.

In addition, the new owner may run out of money to keep the business alive. In this case, there may be no money left for you if the company goes bankrupt.

Let's say you have two serious offers on the table. One is for a higher amount, but involves a ten-year financing period. The second offer is lower, but pays you upfront. I highly recommend the second option.

In conclusion

Are you ready to sell your business? Don't overcomplicate things; the entire process can be broken down into five simple steps. As I have explained throughout the article, selling takes a lot of time; so be patient, and most importantly, be realistic.

Sometimes, postponing the sale for later is also a good idea. This will give you time to better organize your finances, establish exit strategies... Meanwhile, also take the opportunity to take care of the business. It must be doing well. This will allow it to generate even higher profits. This can only attract potential buyers.

In conclusion, I invite you to use this guide as a reference throughout the entire process. Be sure to follow the advice and best practices that I have outlined above, and I guarantee you maximum purchasing value for your business.